- Juniorstocks.com

- Posts

- Antimony: PDAC's VIP Guest, 2025's Junior Mining Boom, EU Critical Mineral's: Call to Arms

Antimony: PDAC's VIP Guest, 2025's Junior Mining Boom, EU Critical Mineral's: Call to Arms

You're receiving this newsletter as a subscriber to JuniorStocks.com. Join the conversation on our socials below.

Editorial Team

March 07, 2025

Featured Article this week:

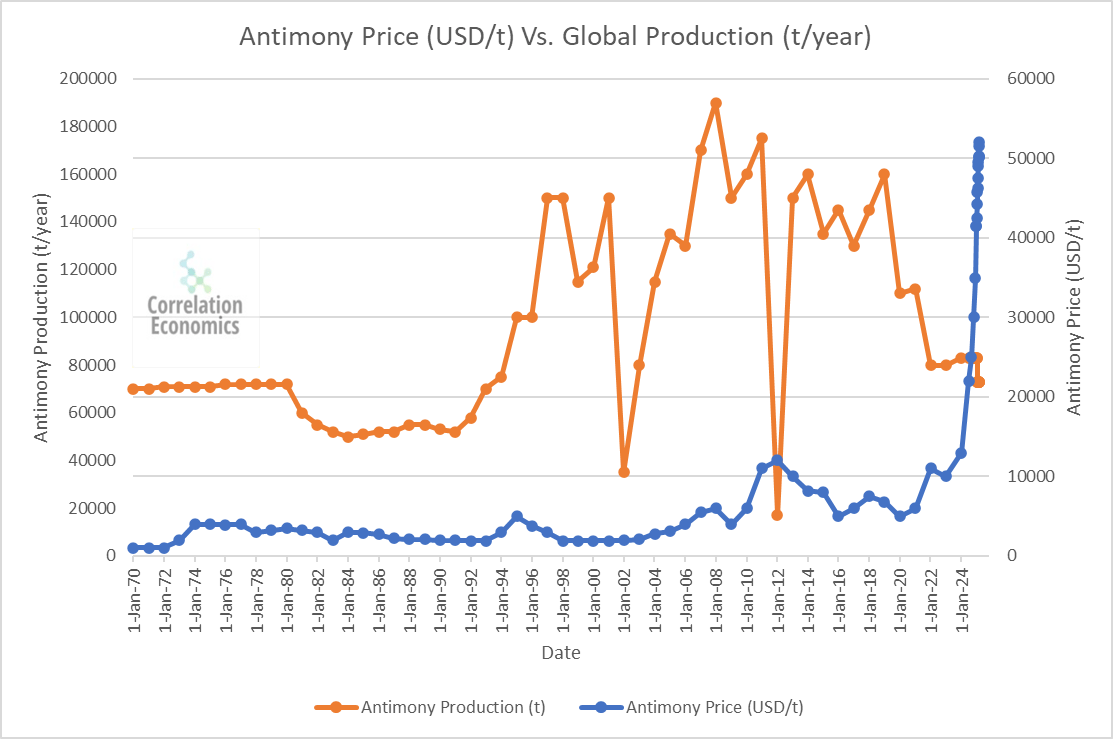

Antimony Takes Center Stage – The hottest topic at PDAC 2025 was antimony, a critical metal used in defense, batteries, and tech. With prices soaring past $50K/ton and China controlling over 50% of global supply, Western nations are looking to Canada to fill the gap.

Tariffs Reshaping Mining – U.S. trade policies and potential tariffs on China are shaking up global supply chains, boosting domestic production opportunities for antimony, copper, lithium, and other critical minerals. Canadian miners are poised to benefit as the West secures local resources.

Mining’s Bull Run Begins – With over 30,000 attendees and growing investor interest, PDAC 2025 showcased the rising demand for critical metals. As China’s dominance weakens, North American miners are gearing up for a profitable decade.

The Junior Mining Boom of 2025: PDAC Analysis

Unleashing the Power of Rising Prices, Smart Financing, and Strategic M&A in the Market

Rising Commodity Prices:

Antimony prices soared 250% in 2024 to $38,000 per tonne by December, fueled by China’s export ban on antimony products, impacting the U.S. military’s 45 million-pound annual demand for munitions and tech. Gold hit record highs (up 38% in 2024) and silver rose 42% with a 140 million-ounce deficit driven by solar demand (up 8% in 2023). However, copper’s 11% rise was partly speculative, and lithium’s projected rebound faces a persistent 80% price drop from 2023 oversupply.

Improved Access to Financing:

State-backed financing for miners grew in 2025, with the U.S. offering a $1.86 billion loan to Perpetua Resources for the Stibnite Gold project (expected to meet 35% of U.S. antimony demand), while Military Metals Corp.’s Slovakian deposit (60,998 tons at 2.478% grade, $3 billion in-situ value) highlights undervaluation at a $35 million market cap.

Historical trends support optimism, with 36% of industry leaders in 2025 citing government support as critical for critical minerals like antimony.

Increased M&A Activity and Strategic Opportunities:

Strategic imperatives fuel M&A, as the U.S. and EU push for domestic supply chains amid U.S.-China tensions. Saudi Arabia’s 10% stake in Vale Base Metals and potential 10% in Pakistan’s Reko Diq project showing Middle Eastern interest.

Chart via. Correlation Economics

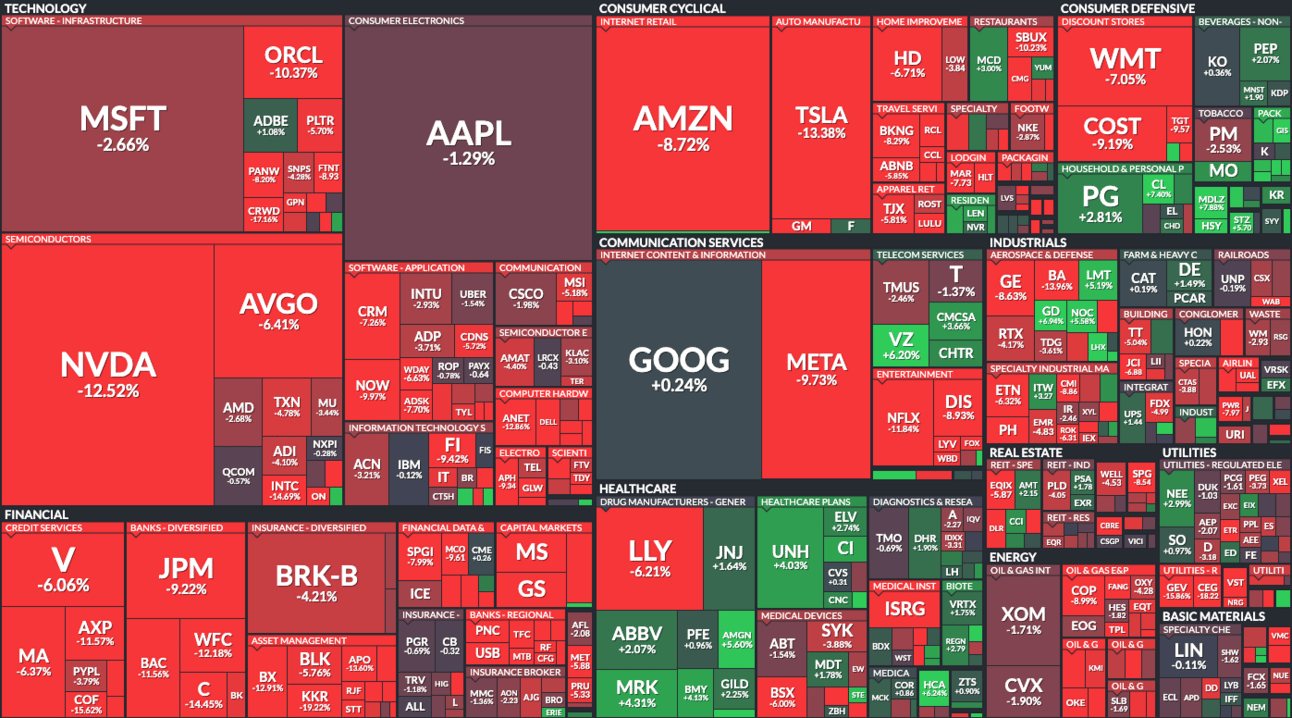

Market Snapshot This Week:

Technology Sector (Software-Infrastructure and Semiconductors): Major companies like MSFT (-2.66%), AAPL (-1.29%), NVDA (-12.52%), and AVGO (-6.41%) show significant declines. This could be attributed to recent market concerns over high valuations in the tech sector, potential regulatory pressures on big tech firms, and softening demand for semiconductors amid economic uncertainty as of early 2025.

Consumer Retail and Internet Retail: AMZN (-8.72%) and WMT (-7.05%) experienced notable drops, possibly due to weaker-than-expected holiday sales reports or shifts in consumer spending patterns towards essential goods, reflecting broader economic slowdown fears reported in recent financial news.

Healthcare and Pharmaceuticals: LLY (-6.21%) and JNJ (+1.64%) show contrasting performances, which might be linked to news about drug pricing regulations impacting LLY negatively, while JNJ benefits from positive clinical trial outcomes or stable demand for healthcare products in early 2025.

All data current as of 12pm EST 03/07/2025

We want your feedback on this week’s market insights! How’d we perform? 📈📉Let us know where we stand! 🚀 |